If Passed, How Would The Responsible Financial Innovation Act Change Digital Asset Broker Reporting Requirements Under the 2021 Jobs Act?

If Passed, How Would The Responsible Financial Innovation Act Change Digital Asset Broker Reporting Requirements Under the 2021 Jobs Act?

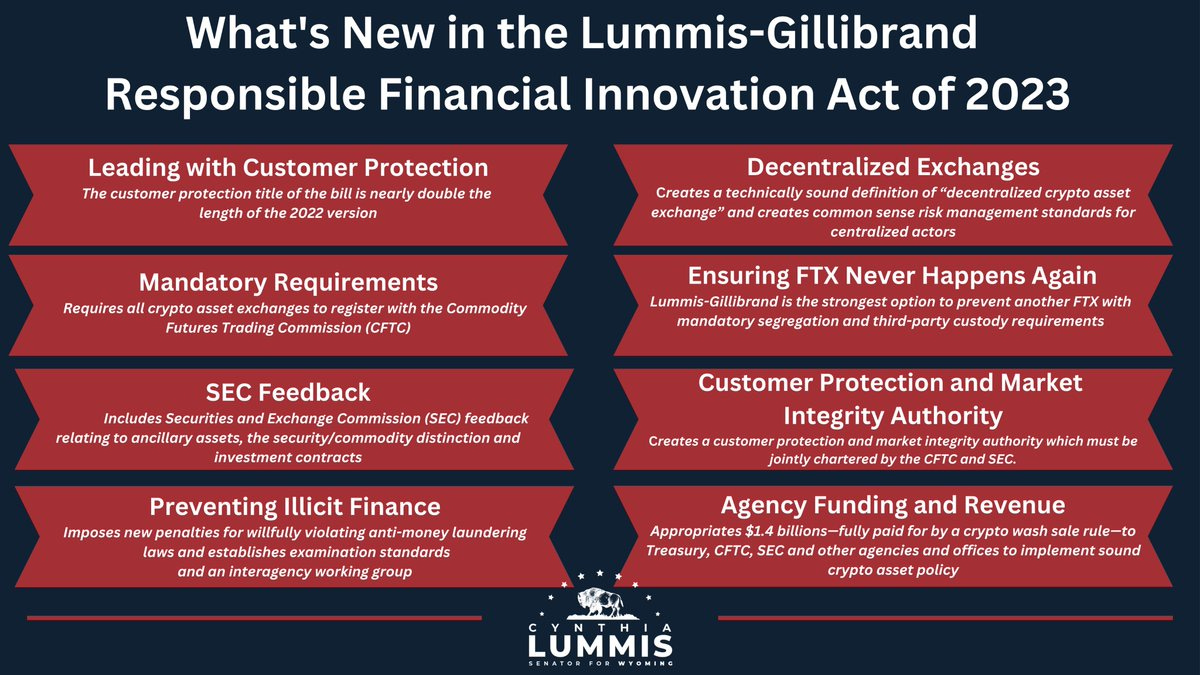

Last week, Senators Cynthia Lummis and Kirsten Gillibrand reintroduced proposed legislation with the aim of bringing regulatory clarity to the digital assets sector. According to a Tweet from Senator Lummis, The Responsible Financial Innovation Act proposes a “strong regulatory foundation” for digital assets that prioritizes “consumer protection” while also cracking down on criminal activity.

I have previously posted about the 2021 Infrastructure Investment and Jobs Act and how Section 80603 of that new law redefines the definition of a digital asset broker and subjects digital asset transfers in excess of $10,000 to enhanced KYC and IRS reporting requirements. Critics in Congress have previously expressed concerns that Section 80603 is poorly drafted and overly expands the definition of a “broker” beyond custodial digital asset intermediaries—thereby creating over expansive regulation of cryptocurrencies and potentially stifling innovation.

Any rulemaking or guidance that fails to appropriately interpret these provisions will damage the privacy of American taxpayers and stifle innovation through rising compliance costs and unnecessary regulatory burdens. We urge Treasury to immediately publish the rules directed under Section 80603 and delay the effective date of Section 80603 to allow market participants to conform to any new requirements. Thank you again for your attention to this important matter. McHenry Letter

How Does Section 80603 Impact Digital Asset Brokers?

The changes taking effect on January 1, 2024 under Section 80603 of the Jobs Act could affect a broad range of entities within the crypto space. Possible sectors of the digital asset space that could be impacted by this new law include:

Cryptocurrency Exchanges: Both centralized and decentralized exchanges may be subject to enhanced KYC/AML reporting requirements under Section 80603.

Crypto Wallet Providers: Digital wallet providers may also fall under this new law. This could include providers of both hardware and software wallets.

Decentralized Finance (DeFi) Platforms: DeFi platforms, despite their decentralized nature, may also be subject to these regulations. This could include lending platforms, decentralized exchanges (DEXs), yield farming platforms, and other DeFi applications.

Cryptocurrency ATM Operators: Operators of cryptocurrency ATMs, which allow users to buy or sell cryptocurrencies, may also need to comply with these regulations.

Peer-to-Peer (P2P) Trading Platforms: P2P platforms that facilitate direct transactions between users without an intermediary may also need to ensure compliance with these new regulations.

Crypto Payment Processors: Companies that process transactions for businesses that accept crypto as a form of payment may also need to comply with reporting requirements under Section 80603 of the Jobs Act.

Initial Coin Offering (ICO) or Token Sale Platforms: Platforms that allow businesses to raise funds through the sale of tokens or coins may also fall under the KYC and AML compliance requirements of Section 80603.

Crypto Custodial Service Providers: Entities that provide custodial services for digital assets could be subject to these regulations.

Blockchain-Based Gaming Platforms: Gaming platforms that involve the use of cryptocurrencies or blockchain technology are also likely subject need to these new regulations.

Traditional Financial Institutions Involved in Crypto: Traditional banks, asset management firms, or other financial institutions that offer crypto services will need to reassess their KYC and AML compliance standards under Section 80603.

How Does Section 80603 Impact Digital Asset Consumers?

The new regulatory changes taking effect on January 1, 2024 under Section 80603 also impact consumer digital asset transactions—particularly those exceeding $10,000. Here are some consumer transactions that are likely to be affected:

Large Digital Asset Purchases/Sales: Any consumer buying or selling digital assets valued at more than $10,000 will likely need to provide additional identifying information. This could impact consumers' willingness to engage in large transactions due to the additional reporting requirements.

Crypto-to-Crypto Exchanges: If a consumer decides to swap one type of cryptocurrency for another and the transaction's value exceeds $10,000, it will likely be subject to these reporting requirements.

Deposits/Withdrawals on Crypto Exchanges: When depositing or withdrawing digital assets worth more than $10,000 on cryptocurrency exchanges, consumers may be subject to additional identification procedures.

Peer-to-Peer Transactions: If a consumer uses a peer-to-peer network to send or receive digital assets, these transactions could be subject to KYC/AML requirements if the transaction exceeds $10,000 in value.

Crypto Payments for Goods and Services: If a consumer pays for goods or services with digital assets, and the transaction value exceeds $10,000, the transaction may require reporting.

DeFi Transactions: Transactions involving lending, borrowing, or staking of digital assets on DeFi platforms could be subject to additional scrutiny if the transaction value exceeds $10,000.

Crypto ATM Transactions: Consumers using cryptocurrency ATMs for transactions exceeding $10,000 will likely have to comply with additional KYC/AML requirements.

Does Section 802 of The Responsible Financial Innovation Act Address These Concerns?

So does the proposed legislation in The Responsible Financial Innovation Act fix any of this? Section 802 of the proposed Act address the definition of digital asset brokers and applicable reporting requirements.

2) FURNISHING OF INFORMATION.—Section 6045A(d) of such Code is amended to read as follows: ‘‘(d) RETURN REQUIREMENT FOR CERTAIN TRANSFERS OF CRYPTO ASSETS NOT OTHERWISE SUBJECT TO REPORTING.—Any broker, with respect to any transfer (which is not part of a sale or exchange executed by such broker) during a calendar year of a covered security which is a crypto asset (as defined in section 9801 of title 31, United States Code) from an account wholly controlled and maintained by such broker to an account which is not maintained by, or an address not associated with, a person that such broker knows or has reason to know is also a broker, shall make a return for such calendar year, in such form as determined by the Secretary, showing the information otherwise required to be furnished with respect to transfers subject to subsection (a). Information reported by brokers under this section shall be limited to customer information that is voluntarily provided by the customer and held by the broker for a legitimate business purpose.’’.

If passed and signed into law as is, Section 802 would also push back the effective compliance date for certain digital asset transfers.

B) DELAYED EFFECTIVE DATE.—Section 80603(c) of the Infrastructure Investment and Jobs Act is amended by striking ‘‘December 31, 2023’’ and inserting ‘‘December 31, 2025’’.

(4) EFFECTIVE DATES.—(A) The amendments made by paragraphs (1) and (2) shall apply to returns required to be filed and statements required to be furnished after December 31, 2025.

(B) The amendments made by paragraph (3) shall take effect as if included in the enact- ment of section 80603 of the Infrastructure In- vestment and Jobs Act.

Here are some observation about how the proposed Act might modify existing laws with respect to how cryptocurrency transactions are monitored and reported, in particular, by brokers.

Definition of Broker: The definition of a broker is clarified as anyone who effects sales of crypto assets at the direction of their customers in the ordinary course of a trade or business. This expands the category of individuals or entities who may be considered brokers for reporting purposes, and could include digital asset exchanges, peer-to-peer trading platforms, and potentially other service providers in the crypto industry.

Crypto Asset Definition: The term 'digital asset' has been replaced with 'crypto asset', and its definition will be as given in section 9801 of title 31, United States Code. This might imply that the focus is specifically on cryptographic assets rather than a broader category of digital assets.

Reporting Requirements: The new law expands the requirement for brokers to file returns for transfers of crypto assets. This includes transfers from an account controlled by the broker to an account not maintained by, or an address not associated with, another known broker. This reporting requirement appears to apply only to customer information that the customer has voluntarily provided and that the broker retains for a legitimate business purpose.

Effective Date: The changes in the broker definition and reporting requirements would take effect for returns required to be filed after December 31, 2025.

Delayed Reporting Requirements: The reporting requirements under section 6050I(d) of the Internal Revenue Code are delayed and certain provisions are removed. This could refer to reporting requirements for cash received in trade or business, or foreign bank and financial accounts.

In summary, if this legislation is passed and signed into law, it would have significant implications for those involved in the buying and selling of cryptocurrencies. It expands the definition of a "broker" and the reporting requirements, which would increase the regulatory oversight over crypto transactions.

Although the Act is intended to help combat tax evasion and ensure compliance, it could also increase operational complexity for digital asset brokers, who will need to closely monitor this legislation and understand the potential impact on their operations and compliance requirements.